Remember how this was supposed to be the Hot Rate-Cut Summer?

Sigh.

Despite falling gas prices, economists and Fed watchers remain concerned that stubborn sticky inflation driven by rising service costs and solid wage growth could persist through the year-end. This underlying pressure may compel the Kevin Warsh-led Federal Reserve to hold interest rates higher for longer to fully cool the economy.

That may also include interest-rate hikes.

Yes, the narrative around U.S. monetary policy has completely inverted. With May Headline PCE climbing to 4.1% and core PCE hitting 3.4%, economists are no longer asking “‘When the Fed will cut” but rather “How soon it will hike?”

Federal Reserve Bank of Minneapolis President Neel Kashkari, a voting member of the FOMC, said June 26 that signs of widespread inflation led him to pencil in one interest-rate increase for this year in the Fed’s June 16-17 economic projections or “dot plot.”

“I’m concerned about inflation, and it’s not only tied to what’s happening in the Middle East, it’s just the impression of broader inflationary pressures in the economy,” Kashkari said in an interview with Bloomberg News.

The CME FedWatch Tool shows significant rate hike shift

The widely-watched CME Group FedWatch Tool showed expectations for a renewed tightening focused on the possibility of interest-rate hikes surged dramatically over the last week.

- July FOMC Meeting: The baseline expectation is still a hold at roughly 64.6% but a surprise summer hike is pulling a 35% chance.

- September FOMC Meeting: A rate hike is now the baseline market expectation with the CME FedWatch Tool pricing in a 70% probability of a 25-basis-point increase to a target rate of 3.75%-4.00%.

- December FOMC Meeting: The probability of at least one rate hike sits at a staggering 86%, up significantly from late spring.

As I reported, big banks including Bank of America and Goldman Sachs aggressively shifted their forecasts, removing all previously expected rate cuts for the remainder of the year. BofA explicitly called for multiple hikes to “bring down the hammer” on sticky services and tariff-induced goods inflation.

“In his press conference last week, Fed Chair Kevin Warshacknowledged that inflation has exceeded the FOMC’s target for more than five years and committed the Fed to restoring price stability. Accordingly, we remain inclined to expect at least one rate hike before year-end, with July a live possibility,’’ according to a note by Yadreni Research emailed to TheStreet.

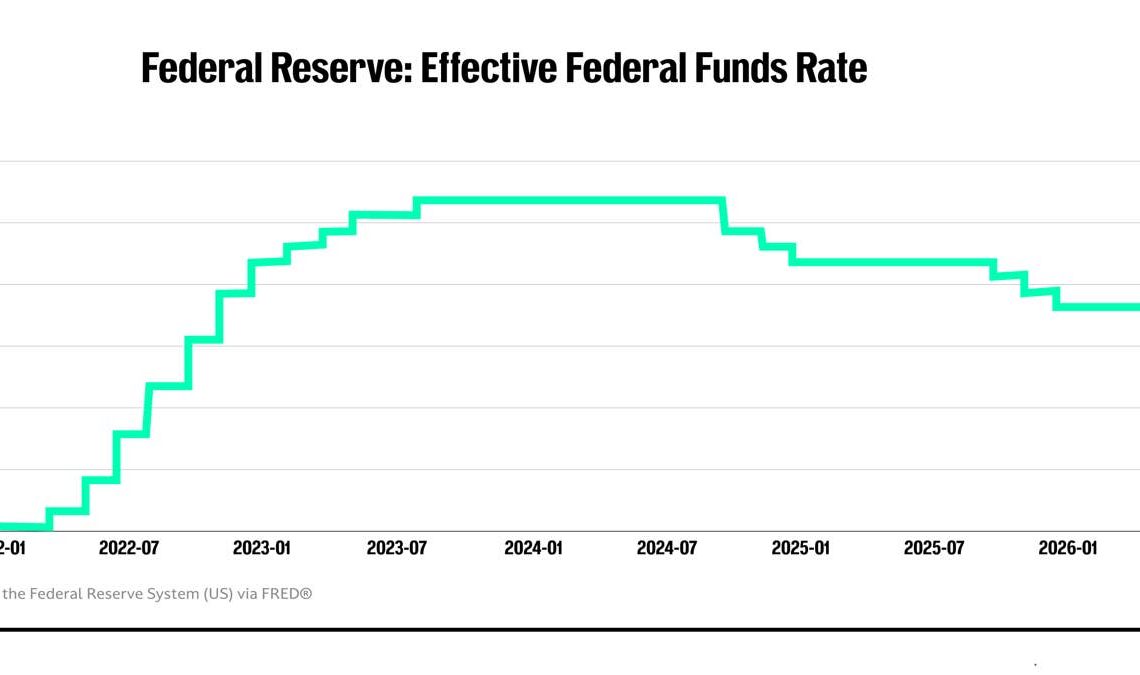

FRED Economic Data/TheStreet

How an interest-rate hike will impact consumers

Most credit cards carry variable Annual Percentage Rates (APRS) tied directly to the Fed’s prime rate. If the Fed hikes rates by 25 or 50 basis points later this year, borrowing costs will climb almost immediately and increase the cost of carrying a balance.

Fixed-rate mortgages track long-term Treasury yields rather than the Federal Funds Rate but mortgage rates will still face renewed upward pressure. Prospective homebuyers and sellers can expect mortgage rates to remain sticky or edge higher, further squeezing housing affordability.

As far as auto loans and personal credit, financing a new or used vehicle will become more expensive and potentially cool consumer demand for big-ticket items.

There is a silver lining for consumers. Yields on High-Yield Savings Accounts (HYSAs), Certificates of Deposit (CDs), and money-market funds will remain elevated or tick higher, rewarding cash savers with strong risk-free returns.

How a possible interest-rate hike will impact investors

For stocks, higher rates increase the discount rate used to value future cash flows which typically pressures equity valuations especially high growth tech and speculative stocks. Companies with heavy debt loads will also face steeper refinancing costs potentially crimping corporate earnings.

With bonds, as a fundamental rule, bond prices move inversely to yields. So a hawkish pivot means yields on the two-year and 10-year Treasury will push higher causing capital losses on existing lower-yielding bonds in your portfolio. However, it also opens up opportunities to lock in higher income on new debt purchases.

The sudden transition from anticipating rate cuts to preparing for rate cuts creates a regime shift. Investors can expect heightened volatilityas Wall Street rapidly reprices classes to adjust to a “higher-for-even-longer’’ interest-rates reality.

Fed keeps rates steady so far this year

The FOMC voted 12-0 June 17 to hold the benchmark Federal Funds Rate steady at 3.50% to 3.75%.

“They’re playing for time,” said Jonathan Hill, head of inflation research strategy at Barclays told The New York Times. “Inflation expectations are tame because the market is anticipating the Fed to hike if needed.”

Policymakers had cut rates by 25 basis points at its last three meetings of 2025 to shore up the softening labor market.

Related: BofA flips the script with bombshell Fed interest-rate outlook

These “insurance” cuts stopped after the majority of policymakers decided the risk from higher prices was outweighing signs that the jobs market was stabilizing.

The funds rate is the interest rate at which banks lend balances at the Federal Reserve to other banks overnight. It triggers the cost of short-term borrowing across the U.S. economy.

Fed’s dual mandate requires a tricky dance

The Fed’s dual mandate from Congress requires maximum employment and stable prices.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

“How do we get inflation back down in a reasonable period of time without doing a lot of damage to the labor market?” Kashkari said. “That’s the challenge that we’re wrestling with.”

Inflation expected to continue to rise through the end of the year

The May Personal Consumption Expenditures, the Fed’s current preferred inflation gauge, marked the highest annual print since early 2023 when it showed Headline PCE (Year-over-Year) at 4.1%, up from 3.8% in April.

- Headline PCE (Month-over-Month): 0.4%, a slight rise from April.

- Core PCE (Year-over-Year, excluding food and energy): 3.4%, a tad higher than April.

- Core PCE (Month-over-Month): 0.3%, held steady with market expectations.

The biggest jump came in May’s consumer spending or nominal PCE at 0.7% at $156.1 billion. Adjusted for inflation, Real PCE rose by 0.3%

The Cleveland Fed had modeled year-over-year headline PCE at 3.97%, up from April’s 3.8%.

Poll: Economists raise inflation forecasts for rest of the year

According to a new Bloomberg poll released June 26, economists raised their forecasts for Core PCE excluding food and energy to rise 3.2% in the fourth quarter from a year earlier. Estimates for overall inflation were little changed at 3.5%.

The poll also boosted estimates for job creation, scrapping the chance of a Federal Reserve interest-rate cut until well into 2027.

“This is a healthy consumer, but the broader macro is giving them a bit of hesitation,” Lowe’s Chief Executive Officer Marvin Ellison said, according to Bloomberg.

Related: Goldman hints at Fed’s next interest-rate bet under Warsh